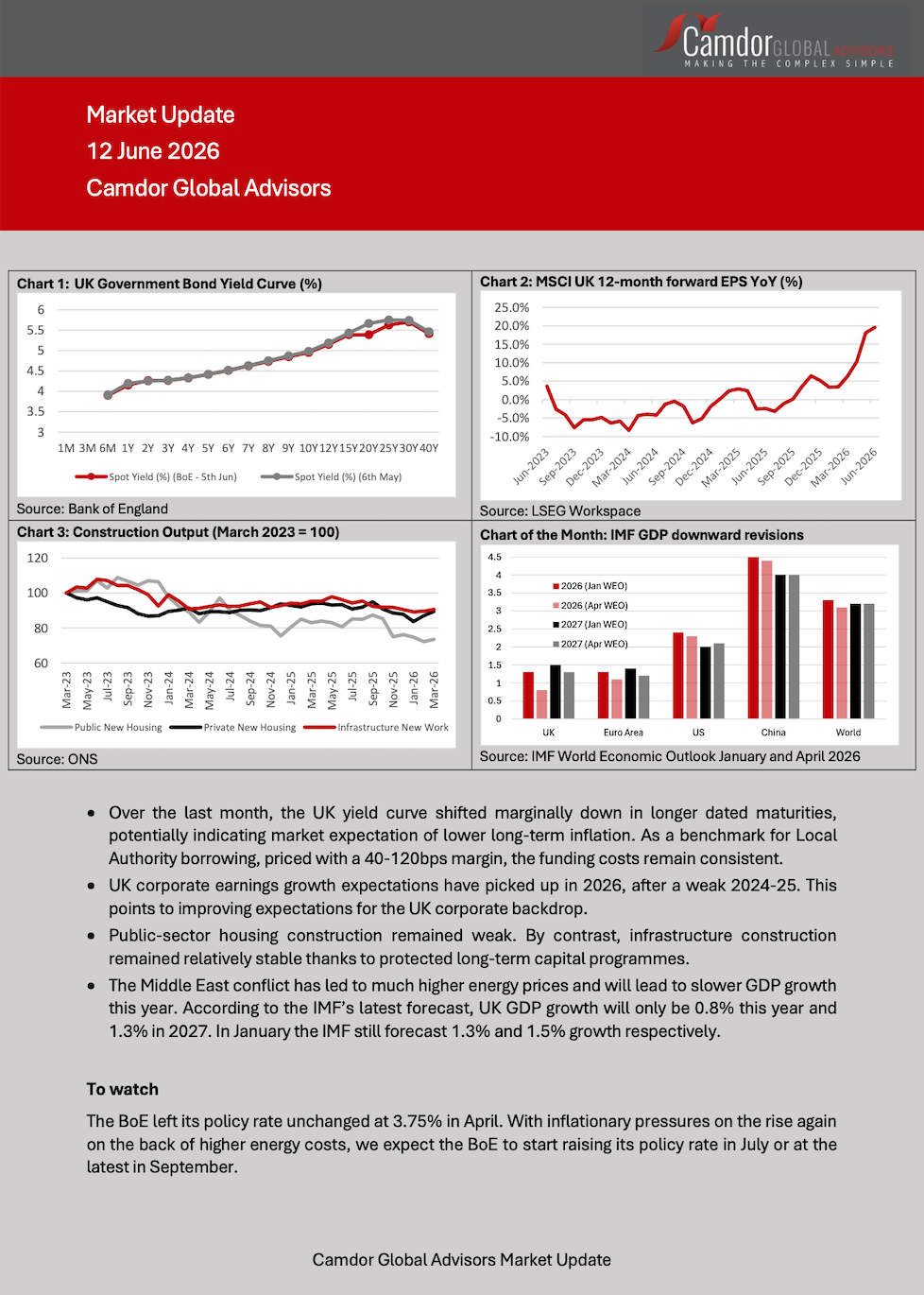

Monthly Market Update – June Edition

We are pleased to announce the launch of our monthly Market Update. The update provides a snapshot of key market developments relevant to Local Authorities.

Crafting Clarity in a

World of Complexity

Learn more about

Camdor Global Advisors

2025 Autumn Budget will provide few positives for local authorities

The Chancellor, Rachel Reeves, will present the Autumn Budget on 26th November. This is an unenviable task given weak growth, geopolitical uncertainties and mounting spending pressures.

The UK government can take some comfort from the fact that other countries are facing similar fiscal challenges. Indeed, among the G7 countries the UK has the second lowest share of government debt in GDP, so shared pain might be half the pain, as the saying goes. The IMF covered this in detail only a few weeks ago: https://lnkd.in/eAYbse7B

Recent developments have offered an additional boost. Updated fiscal assessments suggest the Budget “black hole” in public finances is smaller than previously feared, prompting Rachel Reeves to signal that she will not need to raise income tax after all.

The Institute for Fiscal Studies recently looked at available tax-raising options and dismissed most on fairness, efficiency and other grounds. Raising council tax receipts beyond the already agreed 4.3% annually in future might be an option. This would benefit local authorities unless the central government decided to lower grants in return. But even this would not be without challenges: while the tax take could be boosted by raising tax rates on homes in higher value bands, these bands are still based on property prices when council tax was introduced in the early-1990s. Policymakers have not found the courage to update these bands in more than 30 years, it is unlikely they will find it now. It is no wonder that more and more organisations are arguing for fundamental tax reforms to lift growth and prosperity.

https://lnkd.in/esTcVF-J

For local authorities the autumn budget is unlikely to bring major positive surprises. In mid-October the government confirmed that it would postpone the publication of its eagerly-awaited SEND reform white paper until early-2026, however we remain hopeful that meaningful policy interventions will emerge to address the current shortcomings of the system. Local authorities are not navigating this landscape alone – Camdor Global Advisors continues to support councils with identifying sustainable strategies despite constrained budgets, help to strengthen resilience, and position themselves to take advantage of opportunities as they arise.

https://lnkd.in/eRAjM6AJ

We are pleased to announce the launch of our monthly Market Update. The update provides a snapshot of key market developments relevant to Local Authorities.

The update complements our monthly Pulse, which will continue to focus on policy developments.

Contact Camdor Global Advisors:

Bob Swarup

swarup@camdorglobaladvisors.com

Emerson Chan

emerson@camdorglobaladvisors.com

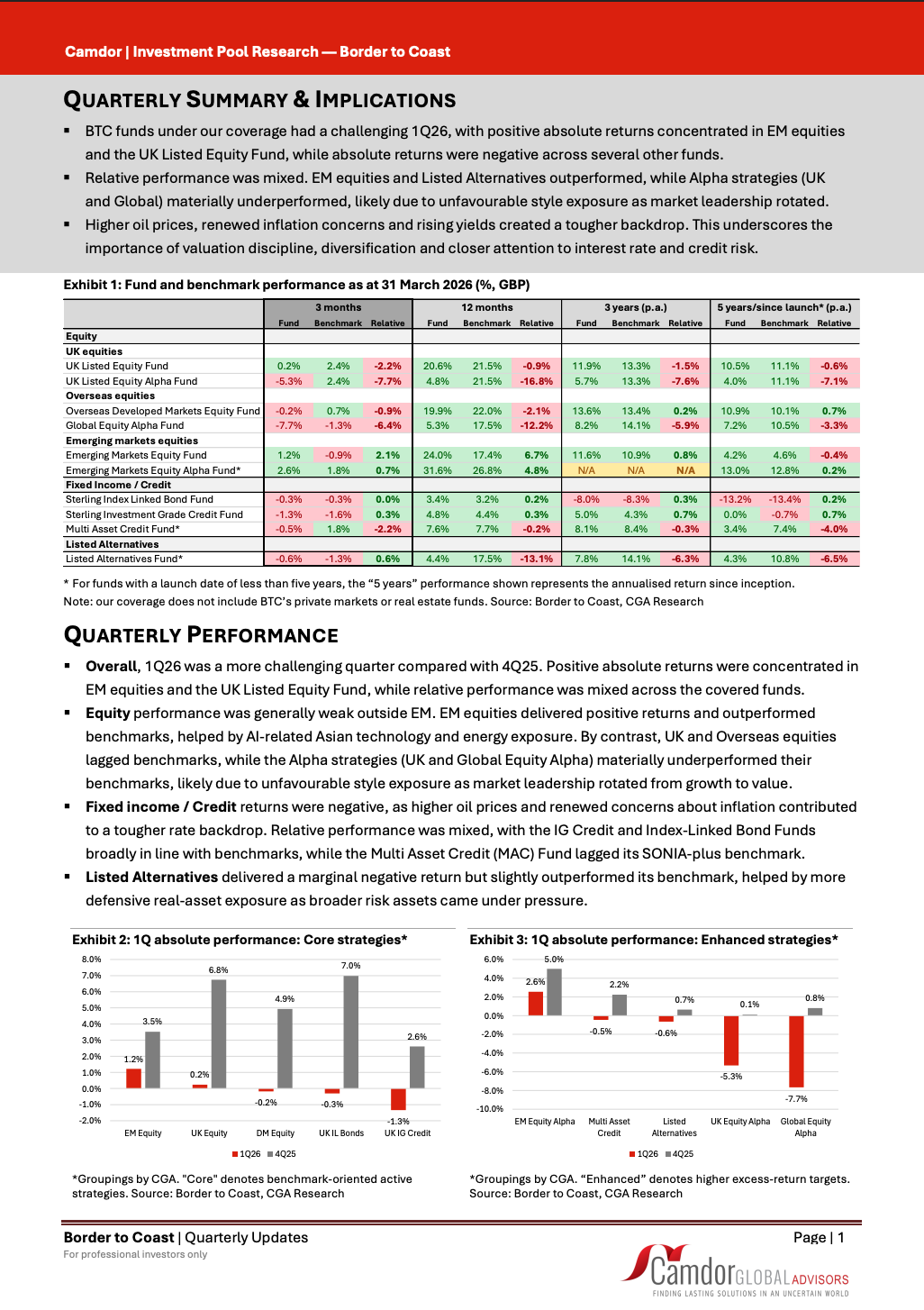

We are pleased to share our latest quarterly review of Border to Coast (BTC), covering 1Q26 fund performance, market backdrop, key risk considerations and discussion questions for LGPS fund oversight.

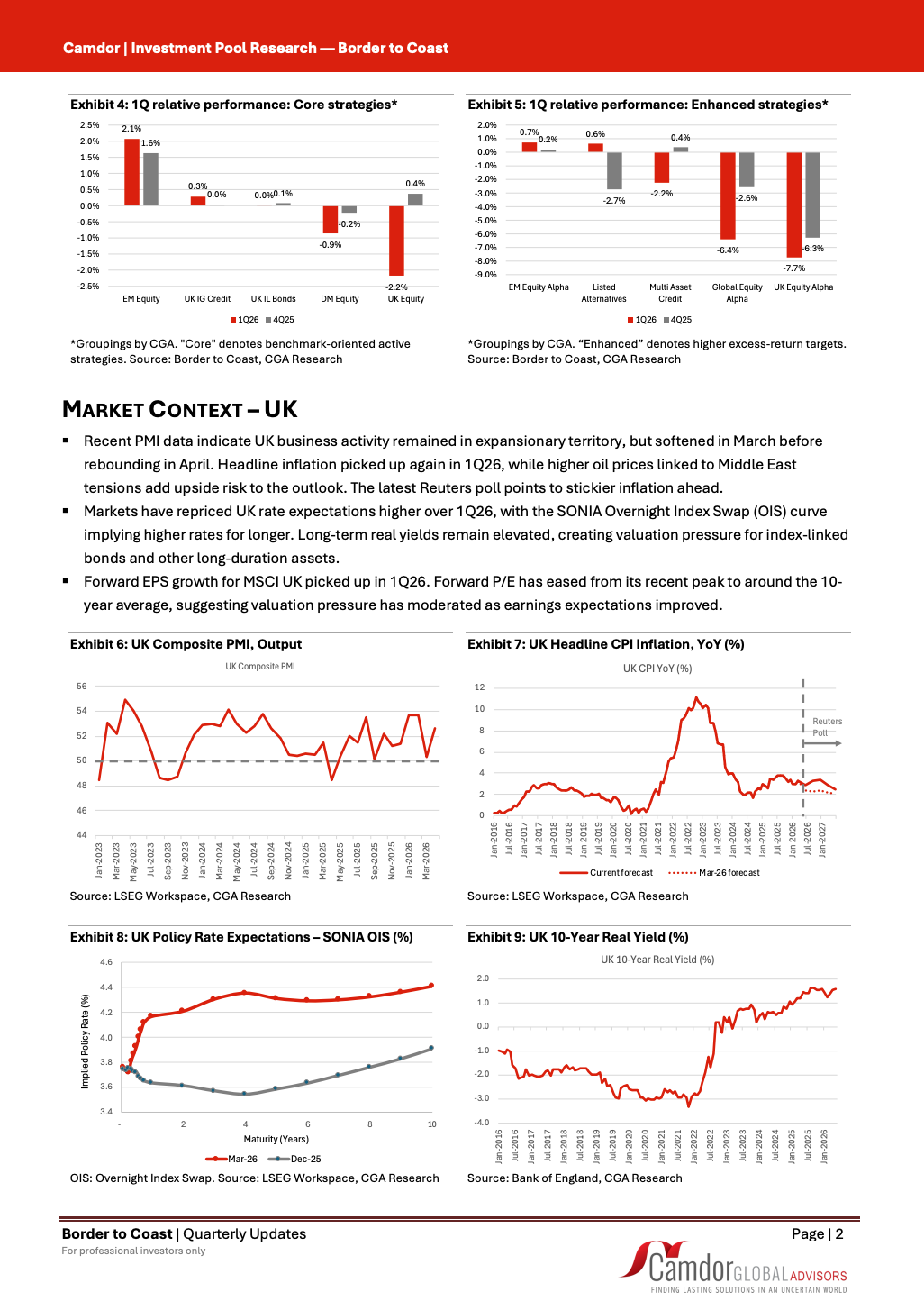

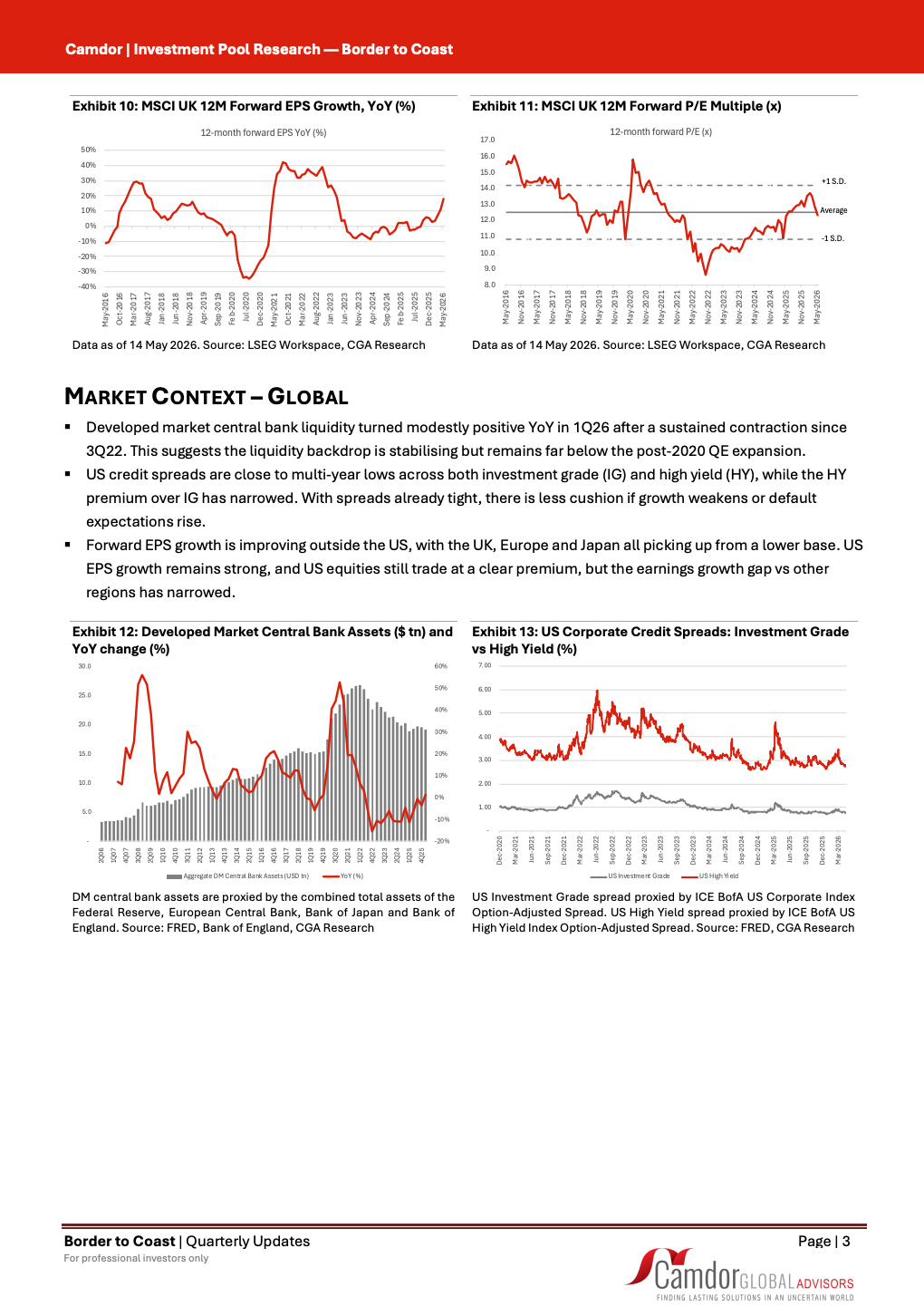

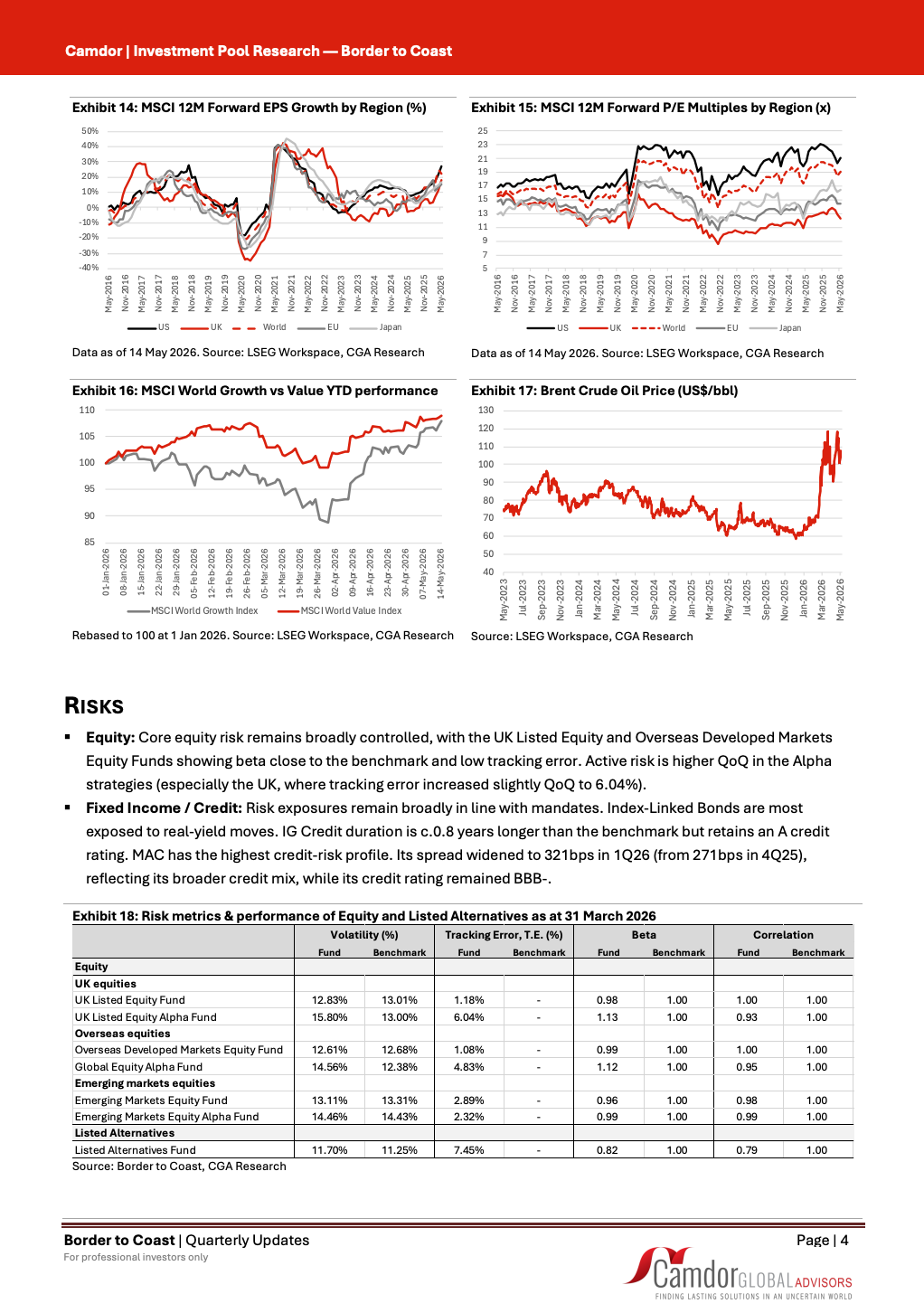

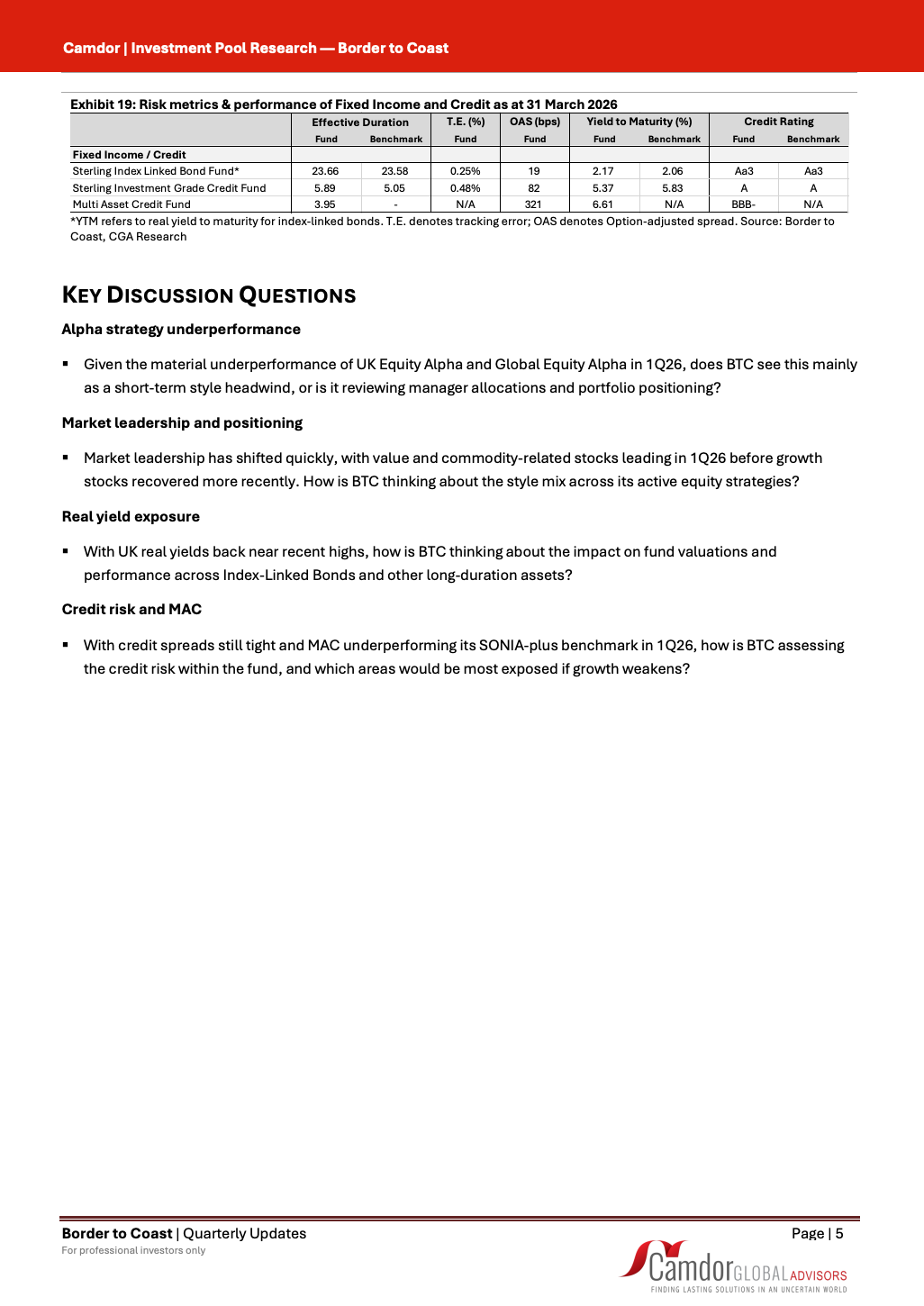

1Q26 was a challenging quarter, with positive absolute returns concentrated in EM equities and the UK Listed Equity Fund, while relative performance was mixed across the covered funds.

The report also discusses higher real yields, tight credit spreads and key questions around style exposure, diversification, interest-rate risk and credit risk.

For professional investors only.

Contact Camdor Global Advisors:

Emerson Chan

emerson@camdorglobaladvisors.com

Vittal Pathi

pathi@camdorglobaladvisors.com

On 21 July 2025, the UK Government made its first major announcement with the establishment of a new pensions commission that could reshape the country’s approach to retirement saving.

Amid the usual political noise from Westminster, this stands out for its potential to deliver lasting structural change and to redefine the state’s role in securing adequate incomes for future pensioners.

The new commission has been tasked with “finishing the job” started by its predecessor in the early 2000s. That earlier body recommended the introduction of workplace pensions with auto-enrolment, one of the most widely cited applications of behavioural economics in UK policymaking. This reform brought millions into pension saving, yet contribution rates remain too low to ensure adequate incomes in later life. The commission will now explore how to increase contributions and strengthen long-term sustainability.

It will also feed into a parallel review of the State Pension age, which will look at international models where pension age automatically adjusts in line with life expectancy. Bob Swarup and Frank Eich analysed similar proposals in 2009, in the wake of the first pensions commission, and their work may be worth revisiting.

The second announcement came with the publication of Sir Jon Cunliffe’s report on the future of the water sector in England and Wales. Sir Jon, a former Second Permanent Secretary to HM Treasury and Deputy Governor of the Bank of England, stresses that the supply of clean water is fundamental to the functioning of society. For this reason, it is often delivered by the public sector, as is the case in Scotland and Northern Ireland. In England and Wales, however, the sector was privatised in the 1980s, with the Government’s role confined to economic regulation via Ofwat.

Sir Jon concludes that this framework has failed to deliver and recommends a fundamental “reset” of the sector. Central to his proposals is the replacement of Ofwat with a new, more integrated regulator and supervisor. This new body would combine oversight of investment, daytoday operations, and longterm resilience.

These policy announcements come at a time when public finances are under sustained pressure. In this context, the Government is focused on two priorities. The first is to contain growth in state pension expenditure, since large increases in annual spending would add strain to the national budget. The second is to fix problems in struggling private utilities by improving regulation and management, thereby avoiding the high costs of taking them into public ownership.

However, the return of parts of the rail network to public ownership illustrates a gradual shift in the balance between public and private provision.

Whether the pensions commission and water sector reforms deliver meaningful change or remain at the level of consultation will hinge on political will and fiscal space.

For now, they are clear signals of where government priorities may be heading and will be closely watched by markets and policymakers alike.

On 21 July 2025, the UK Government made its first major announcement with the establishment of a new pensions commission that could reshape the country’s approach to retirement saving.

Amid the usual political noise from Westminster, this stands out for its potential to deliver lasting structural change and to redefine the state’s role in securing adequate incomes for future pensioners.

The new commission has been tasked with “finishing the job” started by its predecessor in the early 2000s. That earlier body recommended the introduction of workplace pensions with auto-enrolment, one of the most widely cited applications of behavioural economics in UK policymaking. This reform brought millions into pension saving, yet contribution rates remain too low to ensure adequate incomes in later life. The commission will now explore how to increase contributions and strengthen long-term sustainability.

It will also feed into a parallel review of the State Pension age, which will look at international models where pension age automatically adjusts in line with life expectancy. Bob Swarup and Frank Eich analysed similar proposals in 2009, in the wake of the first pensions commission, and their work may be worth revisiting.

The second announcement came with the publication of Sir Jon Cunliffe’s report on the future of the water sector in England and Wales. Sir Jon, a former Second Permanent Secretary to HM Treasury and Deputy Governor of the Bank of England, stresses that the supply of clean water is fundamental to the functioning of society. For this reason, it is often delivered by the public sector, as is the case in Scotland and Northern Ireland. In England and Wales, however, the sector was privatised in the 1980s, with the Government’s role confined to economic regulation via Ofwat.

Sir Jon concludes that this framework has failed to deliver and recommends a fundamental “reset” of the sector. Central to his proposals is the replacement of Ofwat with a new, more integrated regulator and supervisor. This new body would combine oversight of investment, daytoday operations, and longterm resilience.

this context, the Government is focused on two priorities. The first is to contain growth in state pension expenditure, since large increases in annual spending would add strain to the national budget. The second is to fix problems in struggling private utilities by improving regulation and management, thereby avoiding the high costs of taking them into public ownership.

These policy announcements come at a time when public finances are under sustained pressure. In this context, the Government is focused on two priorities. The first is to contain growth in state pension expenditure, since large increases in annual spending would add strain to the national budget. The second is to fix problems in struggling private utilities by improving regulation and management, thereby avoiding the high costs of taking them into public ownership.

However, the return of parts of the rail network to public ownership illustrates a gradual shift in the balance between public and private provision.

Whether the pensions commission and water sector reforms deliver meaningful change or remain at the level of consultation will hinge on political will and fiscal space.

For now, they are clear signals of where government priorities may be heading and will be closely watched by markets and policymakers alike.

The April pulse is here!

To view the latest pricing on investments and borrowings, please click here

Brief updates on the macro environment, markets and key ESG developments are below:

Global and UK Growth Outlook deteriorates due to Middle East Conflict

Cost of Living Support Measures Announced

UK Inflation Rises and BoE Rate Update Amid Conflict

Pension Schemes Bill Nears Completion Amid Parliamentary “Ping Pong” Stage

Devolution Reforms for England Continue to Progress

Clean Energy Transition Accelerates

We hope you find this update valuable.

If you have any questions for Camdor Global Advisors, please don’t hesitate to leave a comment down below, get in touch or check out our LinkedIn and website for more information.

We’re always happy to chat and assist where we can.

On 29 April the Pension Schemes Bill received Royal Assent and became law. It brings to a close a policy initiative which started in late 2024 with Chancellor Reeves’ first Mansion House speech.

According to the Government, this is a landmark bill, which will help more than 20 million people better save for their retirement and will boost UK growth. It aims to achieve that by reducing costs and boosting returns. It will also make it easier to consolidate smaller individual pension pots and allow the creation of multi-employer defined-contribution ‘megafunds’. Importantly, after much back and forth with the House of Lords, the Government agreed to tone down its original plans. These would have given it the power to mandate UK pension schemes to invest in private markets, half of this investment being in the UK.

It is good to see these proposed powers watered down. While we can see why the Government might want to steer pension investment to what it might consider to be “good causes”, it really should be for the schemes themselves to decide what is best for their members.

The Bill also put the finishing touches to the consolidation of the Local Government Pension Scheme into a few pools, which the government hopes will lead to economies of scale and generally better outcomes. This consolidation is nearly complete now, with pools already doing most of what they are expected to do. But as local authorities move from trusted and established arrangements involving appointed fund managers and independent advisors to new arrangements centred around powerful pools, they need to remain extra vigilant. Governance issues may emerge as the relationships between stakeholders change.